All Categories

Featured

Table of Contents

Note, nonetheless, that this does not say anything about readjusting for rising cost of living. On the bonus side, even if you presume your alternative would be to purchase the supply market for those 7 years, which you would certainly get a 10 percent annual return (which is much from particular, especially in the coming decade), this $8208 a year would certainly be more than 4 percent of the resulting nominal stock worth.

Example of a single-premium deferred annuity (with a 25-year deferral), with four payment options. Politeness Charles Schwab. The month-to-month payment below is greatest for the "joint-life-only" option, at $1258 (164 percent greater than with the immediate annuity). However, the "joint-life-with-cash-refund" option pays just $7/month much less, and warranties at the very least $100,000 will certainly be paid out.

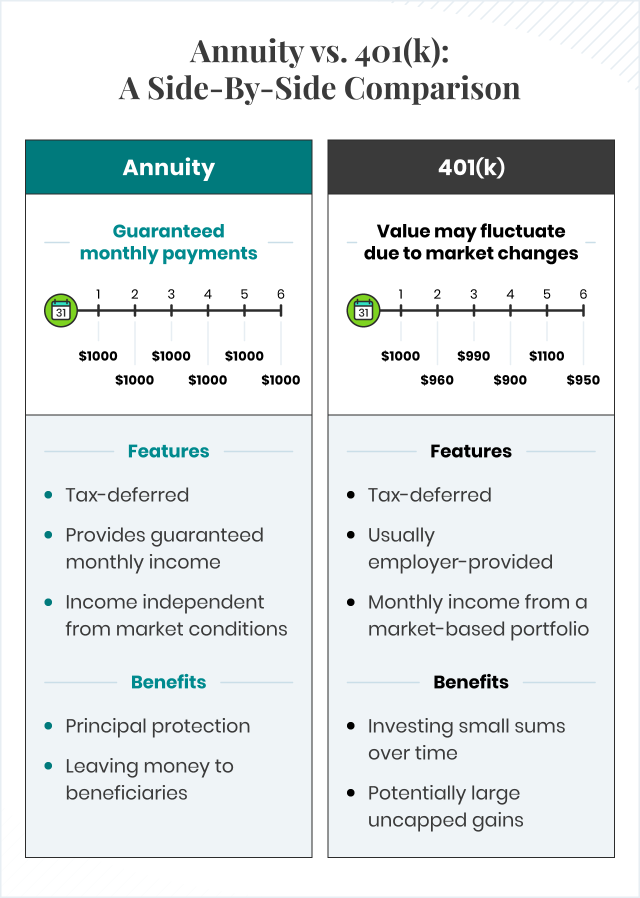

The method you purchase the annuity will certainly establish the solution to that concern. If you purchase an annuity with pre-tax bucks, your premium decreases your gross income for that year. Eventual settlements (regular monthly and/or swelling sum) are taxed as regular earnings in the year they're paid. The benefit here is that the annuity may let you defer taxes beyond the IRS payment limits on Individual retirement accounts and 401(k) plans.

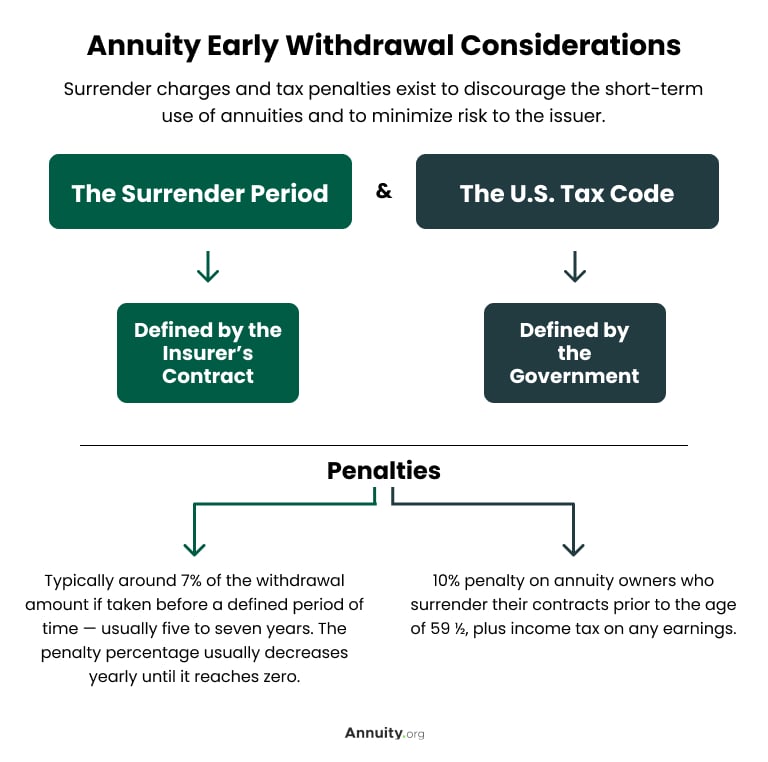

According to , acquiring an annuity inside a Roth strategy results in tax-free payments. Purchasing an annuity with after-tax bucks beyond a Roth causes paying no tax on the portion of each repayment attributed to the original premium(s), but the staying section is taxable. If you're setting up an annuity that starts paying prior to you're 59 years of ages, you might have to pay 10 percent very early withdrawal penalties to the internal revenue service.

What should I look for in an Fixed Annuities plan?

The consultant's very first step was to create a thorough economic plan for you, and after that explain (a) how the suggested annuity matches your total strategy, (b) what options s/he taken into consideration, and (c) how such alternatives would or would not have led to lower or greater payment for the consultant, and (d) why the annuity is the superior choice for you. - Annuity interest rates

Certainly, an advisor may attempt pressing annuities also if they're not the most effective suitable for your scenario and goals. The factor could be as benign as it is the only product they offer, so they fall target to the typical, "If all you have in your tool kit is a hammer, quite quickly everything starts resembling a nail." While the advisor in this situation may not be dishonest, it increases the threat that an annuity is a bad selection for you.

How do I apply for an Flexible Premium Annuities?

Considering that annuities usually pay the agent selling them much greater payments than what s/he would receive for spending your money in shared funds - Long-term care annuities, allow alone the absolutely no commissions s/he would certainly obtain if you purchase no-load shared funds, there is a large motivation for representatives to push annuities, and the much more complicated the much better ()

A deceitful advisor recommends rolling that amount into new "better" funds that just happen to lug a 4 percent sales lots. Consent to this, and the advisor pockets $20,000 of your $500,000, and the funds aren't likely to execute much better (unless you selected much more inadequately to begin with). In the exact same example, the expert could guide you to acquire a challenging annuity keeping that $500,000, one that pays him or her an 8 percent payment.

The advisor hasn't figured out just how annuity payments will certainly be exhausted. The consultant hasn't divulged his/her payment and/or the fees you'll be billed and/or hasn't shown you the impact of those on your eventual settlements, and/or the compensation and/or charges are unacceptably high.

Present rate of interest prices, and thus projected payments, are traditionally low. Also if an annuity is best for you, do your due persistance in comparing annuities marketed by brokers vs. no-load ones sold by the releasing firm.

How do I choose the right Senior Annuities for my needs?

The stream of monthly repayments from Social Security resembles those of a deferred annuity. A 2017 relative evaluation made a comprehensive comparison. The complying with are a few of one of the most significant factors. Considering that annuities are volunteer, individuals acquiring them typically self-select as having a longer-than-average life expectations.

Social Safety and security benefits are completely indexed to the CPI, while annuities either have no rising cost of living protection or at many provide an established portion yearly rise that may or may not make up for rising cost of living completely. This kind of rider, similar to anything else that raises the insurance provider's threat, needs you to pay even more for the annuity, or accept lower repayments.

What are the tax implications of an Income Protection Annuities?

Disclaimer: This write-up is meant for educational functions just, and ought to not be considered monetary guidance. You must consult a monetary expert before making any kind of major financial decisions. My occupation has actually had several uncertain weave. A MSc in academic physics, PhD in speculative high-energy physics, postdoc in bit detector R&D, study position in experimental cosmic-ray physics (consisting of a number of brows through to Antarctica), a brief job at a little design solutions company sustaining NASA, followed by starting my own little consulting technique sustaining NASA projects and programs.

Since annuities are meant for retired life, taxes and fines might use. Principal Security of Fixed Annuities.

Immediate annuities. Used by those that want reliable income promptly (or within one year of purchase). With it, you can customize earnings to fit your requirements and create revenue that lasts permanently. Deferred annuities: For those that intend to expand their money with time, however agree to delay accessibility to the money till retirement years.

Tax-efficient Annuities

Variable annuities: Provides better possibility for development by spending your money in financial investment choices you choose and the ability to rebalance your profile based upon your preferences and in such a way that straightens with changing monetary objectives. With fixed annuities, the firm invests the funds and offers a rates of interest to the client.

When a fatality insurance claim takes place with an annuity, it is important to have a called recipient in the agreement. Various choices exist for annuity fatality advantages, relying on the contract and insurance provider. Selecting a reimbursement or "duration certain" option in your annuity supplies a fatality advantage if you pass away early.

Who should consider buying an Flexible Premium Annuities?

Naming a recipient various other than the estate can assist this procedure go a lot more efficiently, and can help guarantee that the profits go to whoever the individual desired the cash to go to rather than going with probate. When present, a fatality advantage is instantly consisted of with your agreement.

{kind=link}

Table of Contents

Latest Posts

Highlighting the Key Features of Long-Term Investments A Closer Look at How Retirement Planning Works What Is the Best Retirement Option? Advantages and Disadvantages of Choosing Between Fixed Annuity

Understanding Fixed Vs Variable Annuities A Closer Look at Fixed Annuity Vs Equity-linked Variable Annuity Defining the Right Financial Strategy Features of Variable Annuity Vs Fixed Annuity Why Choos

Decoding How Investment Plans Work Key Insights on Your Financial Future What Is the Best Retirement Option? Advantages and Disadvantages of Different Retirement Plans Why Indexed Annuity Vs Fixed Ann

More

Latest Posts